“China’s PMIs drop in January, raising concerns about Q1 2025 growth and the effectiveness of stimulus measures.”, — write: www.fxempire.com

![]()

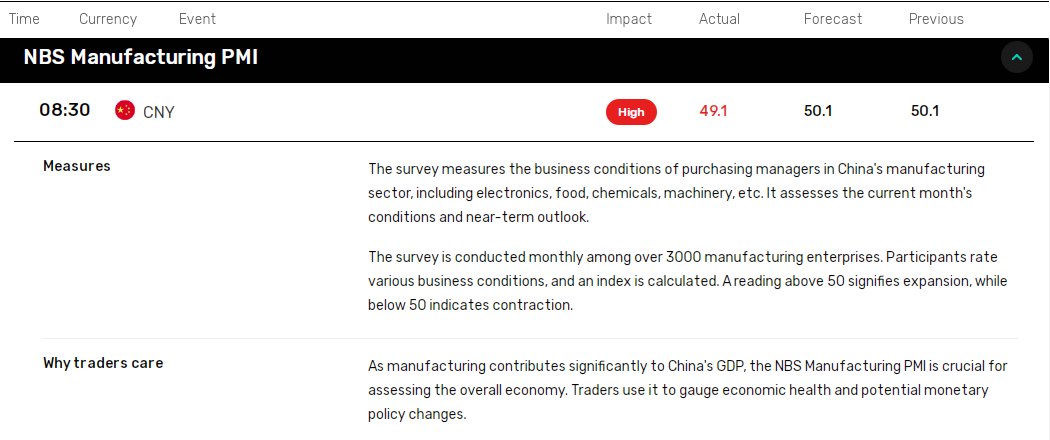

- China’s NBS Manufacturing PMI fell to 49.1 in January, signaling the first contraction since September.

- Non-Manufacturing PMI declined to 50.2, raising concerns over the transition to a consumption-driven economy.

- January’s PMIs highlight challenges in sustaining economic momentum despite 5.4% GDP growth in Q4 2024.

In this article:

China’s National Bureau of Statistics (NBS) Manufacturing PMI dropped from 50.1 in December to 49.1 in January. Services sector activity also waned, with the Non-Manufacturing PMI falling to 50.2 in January, down from 52.2 in December.

The contraction across China’s manufacturing sector and a stalling services sector could raise concerns about the effectiveness of stimulus measures. China’s economy expanded by 5.4% in Q4 2024, up from 4.6% in Q3 2024. However, January’s private sector PMIs suggested a marked loss of momentum going into Q1 2025.

This slowdown may affect China’s labor market, household incomes, and consumer sentiment. Deteriorating consumer sentiment may undermine Beijing’s stimulus efforts aimed at boosting consumption.

January’s figures also highlighted potential front-loading ahead of Trump’s inauguration and tariffs on Chinese goods.

“Conversation with China’s Xi went fine. Would rather not have to use tariffs over China.”

The NBS PMI primarily reflects activity in large state-owned enterprises across the country. In contrast, the Caixin PMI focuses on small- to mid-sized firms, particularly in coastal regions, making it a more comprehensive indicator of private sector performance.

Looking Ahead While China’s stimulus measures may stabilize regional markets, investors should monitor trade developments, inflation trends, and monetary policy signals. A cautious approach remains essential amid lingering uncertainties. Discover strategies to navigate this week’s market trends here.

About the Author

With over 28 years of experience in the financial industry, Bob has worked with various global rating agencies and multinational banks. Currently he is covering currencies, commodities, alternative asset classes and global equities, focusing mostly on European and Asian markets.

Advertisement