“This is no longer a trend, it is an infrastructural shift. With annual growth of 106%, cryptocards are no longer just used to spend small profits: they are now competing with global P2P payment volumes. An $18 billion market analysis that will redefine your banking relationship. This article is brought to you by 21M ⭕, the crypto investing community behind 25% Club. This article […]”, — write: businessua.com.ua

This is no longer a trend, it is an infrastructural shift. With annual growth of 106%, cryptocards are no longer just used to spend small profits: they are now competing with global P2P payment volumes.

An $18 billion market analysis that will redefine your banking relationship.

This article is brought to you by 21M ⭕, the crypto investing community behind 25% Club.

This article contains affiliate links that allow you to support the daily work of the Journal Du Coin teams.

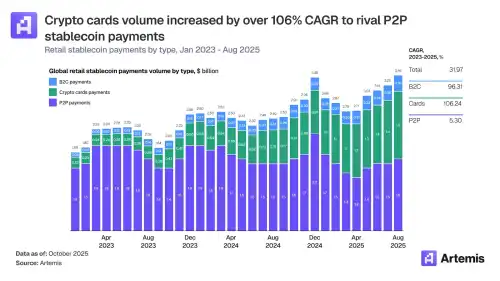

Parabolic adoption For a long time, the “crypto card” was a gadget for the first users. October 2025 data published by Artemis debunks this myth.

Cryptocard payment volumes for the period 2023-2025 experienced a compound annual growth rate (CAGR) of 106.24% . In comparison, P2P (peer-to-peer) payments only grew by 5.30% over the same period.

Figure 1: Crypto card volumes (in green) are growing rapidly and catching up with P2P payments. Source: Artemis.

This graph reveals a fundamental truth: speculative use is giving way to utilitarian use. Users no longer just want to trade; they want live off your digital assets .

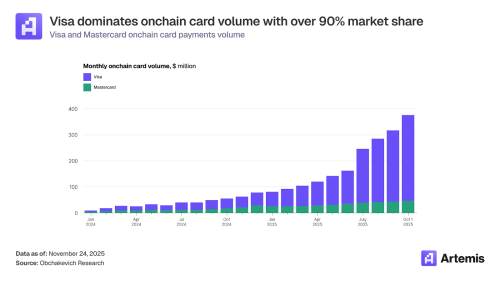

Visa has already won the war Far from being a “rebellious” or “disrupted” ecosystem, this market is now structured by the giants of traditional finance.

Visa and Mastercard go hand-in-hand in the number of programs, having over 130 partnerships each . However, the analysis of trade volumes in the network shows a clear winner.

Figure 2: Visa covers more than 90% of card payment volumes in the network. Source: Artemis.

Visa dominates more than 90% of the market . Why is this data important to you, the investor?

Because it confirms it stability of the system . When the world’s leading payment network blocks the market, the risk of a “shutdown” or sudden ban disappears. Infrastructure exists to last forever.

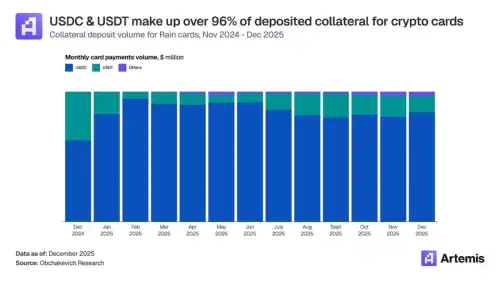

Absolute dominance of the digital dollar What makes these cards work? Contrary to popular belief, this is not Bitcoin (too volatile to pay for coffee).

The report is unambiguous: 96% of the collateral deposited on these cards is USDT and USDC .

Figure 3: USDC and USDT represent the vast majority of funds in use. Source: Artemis.

We are seeing a combination of blockchain liquidity and dollar stability.

The infrastructure has become so complex that it is invisible to the end user. As shown by the technology stack below, players like program managers (Bridge, Baanx) are connecting DeFi and your local bakery’s payment terminal.

Forget your bank: invest your savings in stablecoins For an individual investor, this data is a turning point.

The old model (Sell your cryptocurrency → SEPA transfer → Wait → Bank → Credit card) is outdated. It is slow, unobstructed and financially burdensome.

The new model, confirmed by these $18 billion flows, is as follows: keep your assets in stablecoins and spend them directly.

However, there is one mistake that 90% of users of these cards make: they spend their capital.

They load 1000 USDC and spend 1000 USDC. After all, there is no zero left.

Since the underlying asset is a stablecoin (USDC/USDT), it is eligible for decentralized finance (DeFi) profits.

Instead of leaving that money sitting idle on a card (earning nothing), a savvy investor invests his capital in profitable strategies (safe farming with returns, real world assets).

- Classic scenario: you have 50,000 euros in your bank account. Inflation eats them up.

- 25% club scenario: You invested $50,000 with profitability of 15-20% . This generates ~$8,000 per year or ~$650 per month.

You only need to top up your crypto Visa card with this $650.

Result: you pay for groceries, gas, and restaurants, and at the end of the year, you still have $50,000 left over. That’s how it works” Club 25% .”

That’s what we call it Annuity 3.0 :

This is how we set ourselves this ambitious goal in 15-25% per year transforming this technological revolution on personal income in a safe and diversified way.

👉 Join the 25% club Stablecoins are a topic to be taken seriously right now.

Is your strategy ready?

Please wait…