“The Outcome of German’s Election Makes A Coalition Between the CDU/CSU and the SPD Likely, ALLOWING FOR A RAPID COALITION AGREMENT, TUUGH REFORMS to Germany’s Debt Brake.”, – WRITE: www.fxempire.com

![]()

In this article:

Based on the Results, The Social Democratic Party (SPD) Is Likely to Be the Coalition Partner, whochh Should Accelerate of the Formation of A GOVERNMENT WITH FUWER COMPROMISES NEED-COMPROMISS Coalition Including the Greens.

Germany Needs to Increase Its Room for Budgetary Manoeuvre Not Only Due to the Investment Required to Address Structural Weaknesses in the Economy Buting ALSOBEUSE OF THE POPESSE. HAS INTENSIFIED TO US ADMINISTRATION’S RELUCTision to Continue Finance European Security.

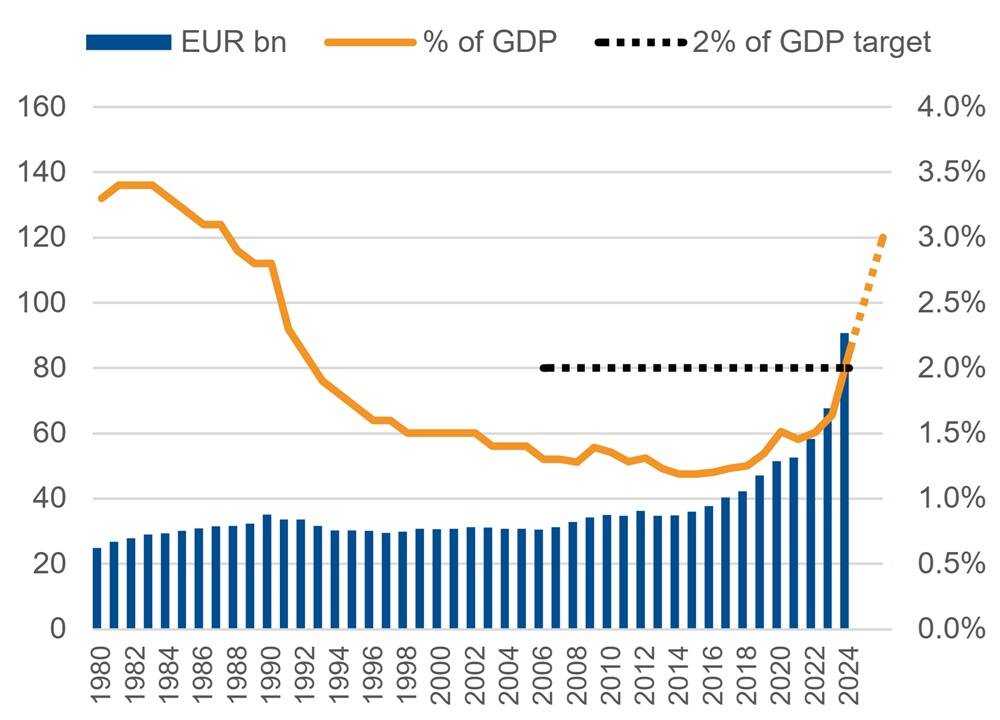

EU Member States in Nato Are Considering Increase Their Commitments On Defence Spending to 3% From 2% Of GDP. This would Leave Many regional sovereigns with a large Budget ShortFall, Weakening Their Credit Profiles.

Once Germany’s Special Defense Expenditure Fund of Eur 100bn is DEPLETED BY the END of 2026, ITS Budgetary Gap would be the largest Among eu Member States at Austnt 13.8%. This Compares with Italy’s and France’s Budgetary Gaps of AROUND 5% OF REVENUE.

The 3% Defense-Spending Target Has Not Been Reached Since the End of the Cold War (Figure 1) and wound require more than one-quarter of Germany’s Current Budget to be allocated to defense. Sufficiently reducing expenditure elsewhere or raising taxes appears highly unlikely in the near term. The incomING GOVERNMENT MAY THEREFORE HAVE TO RELY ON RELIEWED SPECIAL FUNDS, APPROVAL FOR WHICH WOULD REQUIRE A TWO-TIRIRDS Parliamentary Supermajority.

Figure 1: Germany Military Spending Coulding Shift Back to Cold-War Levels

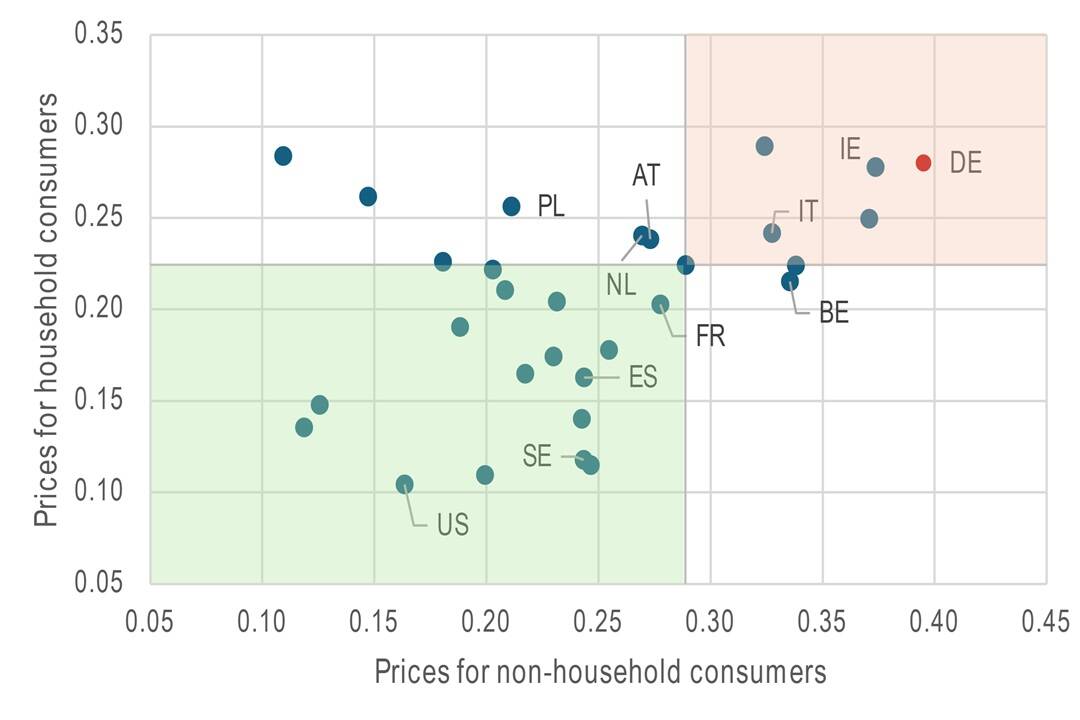

Increased Focus on Lowering Energy Costs from the New Government Germany’s Weak Growth Outlook Reflects ITS Deckling International Competitivens, with High Energy Costs a Particular Problem. After Post-Pandemic Price Surges, Eu Natural Gas Prices in 2024 Remoned Approximately Five Times as High As in The Us. This Compares with Prices Being Approximately 1.8x US PRICES AS OF 2019.

One Way to Address Germany’s High Energy Costs is Through Greater Investments in Power Infrastructure to Better Integrate Growing Volumes of International Solar and Wind-Power. However, Relying Primarily on Private-Sector Commitments Will Keep German Electricity Prices Among The Highest in The EU (Figure 2) AS FIRMS PASS ON COSTS TO END-USERS.

The Significant Investment Needs for the Energy Transition Are Likely to Keep Electricity PRICES ELEVATED COMPEDED COUNTRIES IN Other Eu Countries. Still, The New Government Coulder Raducing Taxes on Electricity and Shifting A Part of the Cost for Upgrading the Grid to the Public Sector. Such Measures Could Be Possible With The Exist DEBT-BRAKE FRAMEWORK, IF Structured As a Financial Transaction.

Figure 2: Household and non-hosehold electricity prices, Eur/kwh

In Addition, Greater Investments in Education and Labour Market Reforms Could Enable Higher WorkForce Participation Among Women and Migrants. Given Germany’s Shortages of Skilled Labour and Significant Demographic Challenge, It Will Also Be Important Menasures to Tigen Immigration Doscoourard Skild

Reducing Bureaucracry and Simplifying Regulation to Support Private Sector Investment Have Been Recognized As Priorities by Most Political Parties, Althoughh Any Implentation of Reformation.

These Structural Reforms Are Critical To Raising Medium-Term Growth. Combined with a potential reform of the debt-Brake ru to the allwhtth-sencing public-sector investment, this wold create addyed-excala to the exaCe-to-help aded the rising. Long-Term Economic Resilience.

For a look at all of today’s Economic Events, Check Out Our Economic Calendar.

Eiko sievert is a senior Director in Sovereign and Public Sector Ratings at Scope Rathings Gmbh.

About the author

Eiko Sievert Is a Senior Director in Scope’s Sopeign & Public Sector Ratings Group, Responsible for Ratings and Research on A Number of Sovereign and Supranational Borrowers.