“Germany needs a stable and reform-oriented government to respond to the impact of US president-elect Donald Trump’s potential policy shifts that will impact Germany’s trade, fiscal and defence policies.”, — write: www.fxempire.com

![]()

In this article:

Some of the adverse implications from a second Trump presidency are likely to take effect at the start of his term in January 2025. Inability by the German government to respond swiftly to some of the forthcoming measures could heighten the country’s persistent structural vulnerabilities that have slowed growth over the past two years.

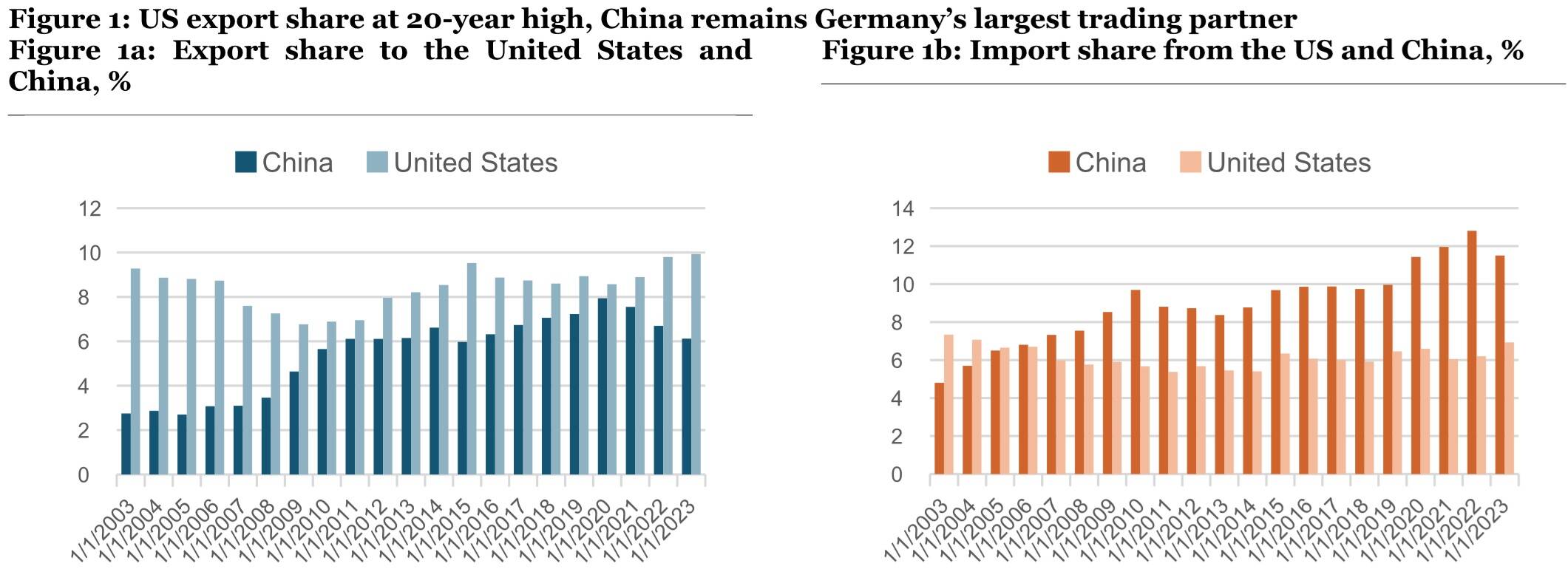

Repercussions of a Trump Presidency Are Wide-ranging The US, Germany’s second largest trading partner after China and largest single export destination, is expected to impose higher import tariffs, which would pose a significant setback for Germany’s export-dependent economy.

Almost 10% of German exports were destined for the US in 2023 – the highest share in more than 20 years. At the same time, the share of exports to China fell from an all-time high of 8% in 2020 to 6% in 2023, partially reflecting the increased competitiveness of China’s manufacturing sector, particularly its automotive sector.

Germany also remains highly reliant on imports from China, which accounted for 11.5% of total imports in 2023. Rising global protectionism and the increasing risk of a US-China trade war will test the resilience of German supply chains over the coming years.

However, additional defence expenditure will be difficult to accommodate despite Germany’s fiscal space, with projected fiscal deficits averaging 1.2% of GDP in coming years and a debt ratio expected to fall below 60% by 2029.

However, a key risk for these potential policy shifts, which would be positive for the German and European growth outlooks, is the increasing parliamentary fragmentation.

Current polls indicate that the two parties at the political extremes, Alternative for Germany and Alliance Sahra Wagenknecht, could win around 25% of the vote. If these parties were to perform better than expected and achieve a blocking majority for constitutional changes of more than 33%, it could further complicate discussions concerning debt-brake changes.

For a look at all of today’s economic events, check out our economic calendar.

Eiko Sievert is a Senior Director in Sovereign and Public Sector ratings at Scope Ratings GmbH.

About the Author

Eiko Sievert is a Director in Scope’s Sovereign & Public Sector ratings group, responsible for ratings and research on a number of sovereign and supranational borrowers.

Advertisement