“Political uncertainty, a challenging fiscal outlook, and the rising divergence in funding conditions between France and other core euro area sovereign borrowers underscore the importance of political stability.”, — write: www.fxempire.com

![]()

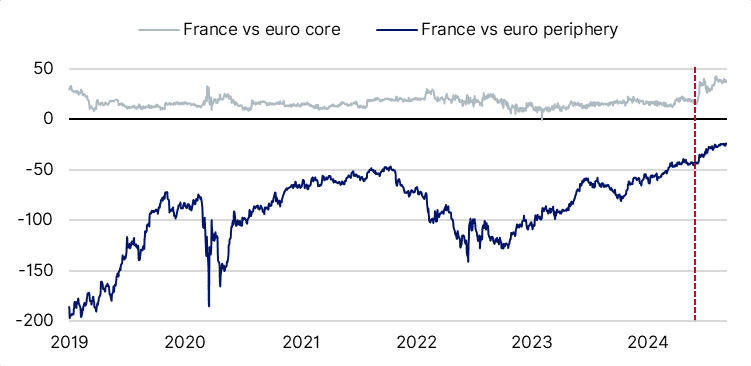

The yield spread between French 10-year government debt and those of other core euro area countries has widened to around 40bp, up from a five-year average over 2019-23 of about 16bp, since President Macron’s decision to call early legislative elections (Figure 1). This points to a moderate, albeit rising, divergence of France’s funding conditions compared with those of AAA-rated sovereigns.

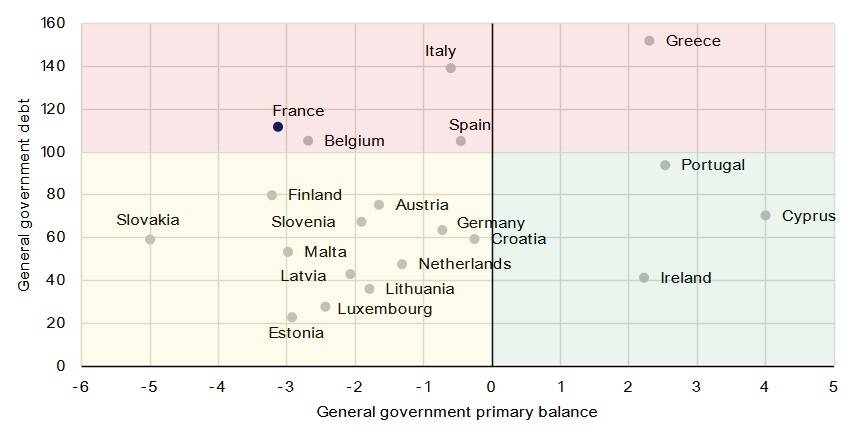

France’s 2024 budget deficit is likely to be revised up to 5.6% of GDP from 5.1% planned in the Stability Programme. This points to another year of fiscal slippage as the 2023 deficit had already been revised to 5.5% of GDP from the planned 4.9%. France is thus set to record the second widest budget deficit among euro area countries, after Slovakia (5.9% of GDP), and significantly above the 3% Maastricht threshold.

Figure 1. France’s funding costs rising vs core euro countries, convergence with that of the euro-area periphery

Spread, 10-year government bond yield, basis points

Figure 2. France runs one of the largest primary deficits

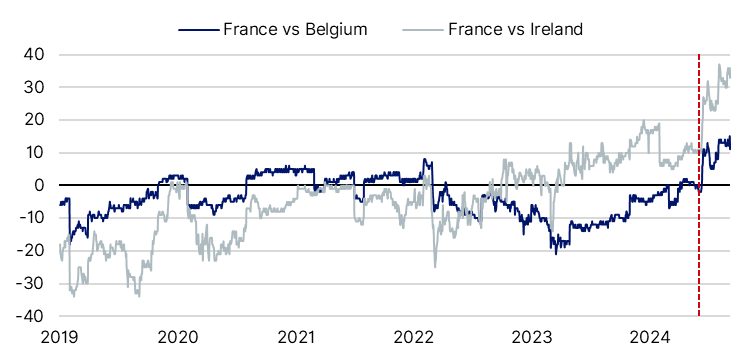

Figure 3. Reversal of France’s spread against Belgium and Ireland

Spread, 10-year government bond yield, basis points

Moreover, France benefits from highly liquid debt markets, a favourable public debt profile, and safe-haven inflows of investors’ “flight to quality” during times of crisis. Still, despite these credit strengths, progress on supply-side reforms and spending cuts are needed to ensure government debt returns to a firm downward trajectory from the 110.6% of GDP level in 2023.

For a look at all of today’s economic events, check out our economic calendar.

Thomas Gillet is a Director in Sovereign and Public Sector ratings at Scope Ratings GmbH, and primary analyst on France’s sovereign credit rating. Brian Marly, a senior analyst at Scope, contributed to drafting this comment.

About the Author

Thomas Gillet is a Director in Scope’s Sovereign and Public Sector ratings group, responsible for ratings and research on a number of sovereign borrowers. Before joining Scope, Thomas worked for Global Sovereign Advisory, a financial advisory firm based in Paris dedicated to sovereign and quasi-sovereign entities.

Advertisement